Your cart is currently empty!

Tag: China

How China Is Rushing To Fill The Gaps Trump Is Creating

America, the leader of the free world, is once again hellbent on abdicating its global leadership responsibilities. Donald Trump is back, and so is his signature foreign policy move—cutting the US off from some key global organisations. He has, just like during his first term, decided that the World Health Organisation (WHO) doesn’t deserve US funding anymore. His reason is the same as before: the WHO did not act right during the Covid-19 pandemic and that it’s bent more favourably towards China.

The American contribution to WHO in 2024 was $950 million. This was nearly 15% of the organisation’s budget, making it the largest single donor out of 194 member countries. So, when Trump pulls out, it’s not just a dent—it’s a crater in the organisation’s budget.

The WHO is funded through two primary sources: assessed contributions, which are mandatory dues paid by the 194 member countries, calculated on factors like a country’s wealth and population, and voluntary contributions, which come from member states, private individuals, philanthropic organisations and other partners. A significant portion of the WHO’s budget relies on voluntary contributions, chiefly the Bill & Melinda Gates Foundation, which provides substantial funding to support various global health initiatives. In fact, the Gates Foundation has pledged to continue to contribute to global health causes.

A Billion-Dollar Challenge To Trump

The WHO, worried but not surprised like last time, has politely asked Trump to reconsider his decision. It says it “plays a crucial role in protecting the health and security of the world’s people, including Americans, by addressing the root causes of disease, building stronger health systems, and detecting, preventing and responding to health emergencies, including disease outbreaks, often in dangerous places where others cannot go”.

There has been a global backlash to the US move. But this one should put the country to shame: a member of WHO staff has embarked on a campaign to raise $1 billion through crowdfunding—just enough to cover what the US contributed in 2024. So far, donations have been only trickling in—ordinary citizens of the world are paying from $1 to $4,000 per person. It’s a noble gesture, a show of defiance against Trump, but let’s be honest. It’s like climbing Mount Everest. The symbolism, though, is powerful. The message to Trump is clear.

The WHO is no stranger to both applause and outrage. It vaccinated over 90% of children in Gaza against polio—commendable indeed, considering it accomplished the feat during the ongoing war in Gaza. It battled the Ebola virus in conflict zones where even armies feared to tread. It has led global vaccination drives that have saved millions of lives. But it has its share of shortcomings and failures too: it botched the early COVID-19 response, hesitating to call out China when the virus first spread, it has been accused of bureaucratic delays that cost lives during major health crises, and though it has launched internal reforms since the end of the pandemic, they are not enough.

Ironically, Trump’s executive order to cripple WHO financially to further his cause of pushing the “America First” agenda may prove counterproductive. By walking away from global commitments, Trump might be winning cheers from his MAGA base, but he doesn’t realise that when the next global health crisis hits, his country might find itself very much alone. And for a country that was once the leader of the free world, that’s quite a downgrade.

Also, what should be more worrying for the US is the possibility that Trump’s action may just open up space for China to step in to fill the gap. Last time Trump pulled this stunt, China rushed in, pledging to increase its voluntary contributions to the WHO. This time, Beijing is still weighing its options.

An Ever-Growing China

The US exiting the WHO and other global agreements and institutions under Trump’s “America First” policy is going to create a power vacuum, which China is sure to quickly move to fill. If this trend continues, Beijing will feel that it would gain the ability to reshape international norms, setting rules that favour its economic, political and ideological interests.

There’s proof to back this. But first let’s look at which treaties and organisations Trump got out of during his first term that led to the US retreating from global leadership:

- World Health Organization (2020): The US left it amid the COVID-19 pandemic, accusing it of being too China-centric

- Paris Climate Accord (2017): The US claimed that it unfairly burdened the US while allowing China to pollute.

- Iran Nuclear Deal (JCPOA) (2018): America’s exit led to Iran’s renewed nuclear activity and increased West Asia tensions.

- Trans-Pacific Partnership (TPP) (2017): The US cancelled a major trade pact designed to counter China’s dominance in Asia.

- UNESCO & UN Human Rights Council (2018): The American withdrawal was due to claims of bias against the US and Israel

- Arms Control Treaties: The US withdrew from the INF Treaty with Russia, increasing global arms race risks

- NATO & G7 Threats: Trump repeatedly threatened to withdraw from NATO, weakening confidence in the alliance

Each of these exits did not necessarily weaken the organisations themselves, but they certainly led to massive uncertainties. Some might argue it reduced US influence and allowed China to step in an effort to fill the leadership vacuum.

Did China Gain From US Withdrawals?

When Trump cut WHO funding in 2020, China stepped up, committing $50 million more to fill the gap. Though the increased amount was far below the US contributions, it allowed Beijing to increase its influence in the organisation, block investigations into COVID-19 origins, and promote its vaccines globally. When Trump withdrew from the Paris Climate Accord, China became the climate leader in climate discussions. Beijing now portrays itself as greener than the US, despite being the world’s largest polluter. Similarly, after Trump unilaterally left the Iran Nuclear Deal, China strengthened ties with Tehran. It also increased oil imports from Iran and expanded economic ties, undermining US sanctions.

Moreover, when Trump withdrew, rather foolishly, from the Trans-Pacific Partnership (TPP), China joined the Regional Comprehensive Economic Partnership (RCEP), now the world’s largest trade pact—without the US being a part of it. The result is that the Asian countries now trade more with China than the US.

China Sets The Agenda

China secured key leadership roles in UN agencies such as the International Telecommunication Union (ITU), which governs internet standards. It uses these positions to push for global acceptance of Chinese tech models, such as surveillance-based governance.

The more Trump withdraws from global agreements and institutions in the name of the “America First” campaign, the weaker it makes his country, because someone else takes its leadership role. That someone else, in this case, will be none other than China. By enhancing its contributions to a large extent, it will surely set global economic rules, trade investment policies favouring state-owned enterprises, and Chinese dominance. It could control global health governance by prioritising Chinese interests, influencing pandemic response and vaccine policies. It will try to shape digital and internet rules by expanding China’s alleged authoritarian “cyber sovereignty” model, limiting online freedoms.

China will expand military alliances by strengthening BRICS and China-led military partnerships to counter US alliances. It will try to dominate climate policies by controlling carbon markets and green technologies while holding the West accountable for emissions.

China Can Be Checkmated

There is still time for influential countries like India and European nations to step up, support the WHO more and prevent China from assuming a dominant decision-making role. Rather than allowing Beijing to expand its influence unchecked, member countries must collectively address WHO’s funding and governance challenges. Mid-sized economies like India and Brazil, along with developed nations, such as the UK, Germany and France, should increase their contributions to maintain a balanced and effective WHO. The organisation’s past success in eradicating smallpox—one of humanity’s greatest achievements—demonstrates that global health cooperation can transcend political divides to protect everyone.

As for the US, I wonder, does MAGA truly make America stronger, or does it isolate the country while China fills the void in global institutions? With each withdrawal—from WHO to climate agreements and beyond—Trump’s America retreats from leadership, leaving a power vacuum that Beijing is eager to exploit. Are we heading towards “America First” or “America Alone”?

(Syed Zubair Ahmed is a London-based senior Indian journalist with three decades of experience with the Western media)

Disclaimer: These are the personal opinions of the author

Real Estate: China’s loss is India’s gain as CapitaLand shifts gears

But on a Friday afternoon last month, ITPB, which is dotted with all kinds of commercial buildings, including a mall, a premium hotel, recreational facilities, and the offices of the world’s biggest multinationals, was teeming with people. Some of the older edifices in the 30-year-old park are now getting a facelift. And in one corner, a massive parking lot has been turned into a construction site, where nearly 2.4 million sq. ft of new office space is coming up.

ITPB epitomizes a larger story that is playing out across India. Office goers are back and demand for offices is booming. And Singapore-headquartered CapitaLand Investment (CLI), which operates ITPB and is its majority owner, is making the most of this renewal as part of a concerted India play.

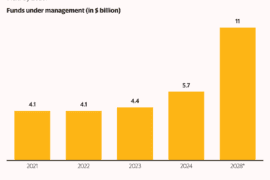

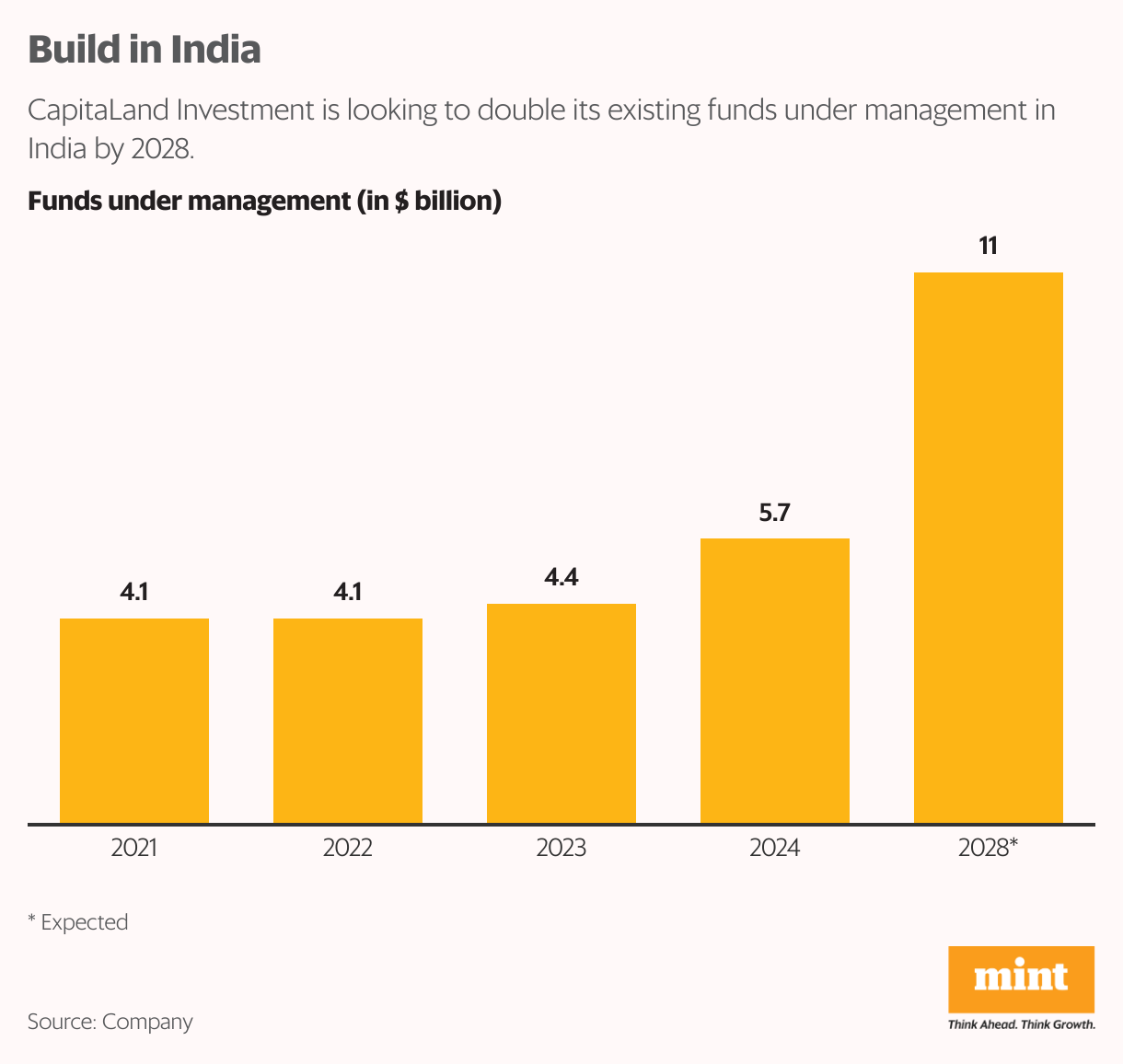

Last September, the Singaporean company announced that it was looking to more than double its $5.7 billion funds under management in India by 2028. The new investments will be in existing businesses—office parks, logistics and industrial real estate, data centres, and lodging—as well as in new areas such as renewable energy and private credit for real estate.

CLI already has a number of commercial projects under construction or in the pipeline in cities across India.

The real estate investor’s decision to have a broader presence in the country has been prompted to a large extent by the growth prospects of the Indian economy. But that isn’t the sole reason. CLI has also been pushed to diversify its Asian investments in the face of mounting challenges in a key market.

Beyond China

The term ‘China + 1’ was coined to describe a business strategy that involves diversifying manufacturing and sourcing beyond China. Drawn by the Asian giant’s low labour and production costs, as well as its enormous domestic market, many multinationals had invested huge sums in the country. But in the wake of trade tensions, increasing labour costs and extended covid lockdowns, many of them made a conscious decision to reduce their dependence on China and find alternative supply chain centres.

While it is not a manufacturer of goods, CLI, part of CapitaLand Group, a diversified real estate conglomerate, has taken a leaf out of the China + 1 playbook. Over the decades, it invested in everything from office spaces to malls in China. The country is, in fact, CLI’s second biggest market after Singapore, its home turf. But China’s real estate crisis, which began in 2021 with a default by housing developer Evergrande Group, has taken a toll on some of those investments.

")

View Full Image

China’s real estate crisis began in 2021 with a default by housing developer Evergrande Group. (Reuters)

Last November, citing the company’s investor day presentation, it was widely reported by foreign media that CLI would moderate its China exposure from 27% of its funds under management to 10-20% by 2028. The reports also noted that the company had warned of likely losses as it sought to emerge from the real estate debacle. While moderating its presence in China, CLI said it would step on the gas in markets such as India, Japan, Korea and Australia.

“Many APAC investors are following the ‘anything but China’ strategy. As a result, investors in Singapore, Japan and even Korea will reallocate capital, a part of which will come to India,” said Shobhit Agarwal, managing director and chief executive at advisory firm Anarock Capital. “Singaporean investors such as CapitaLand Investment, for instance, are looking for deeper value and are taking long-term bets.”

While still making up only a modest part of its overall funds under management, India certainly appears to be a big part of CLI’s plans as it looks to diversify beyond China.

Full speed ahead

Barring a few hotel assets, CLI didn’t have much of a presence in India before 2019. That changed when it merged with Ascendas-Singbridge to create one of the largest real estate groups in Asia. Ascendas, a Singapore government-backed developer, had in fact begun its journey in India in 1994 with ITPB. The tech park in Whitefield had been conceived a couple of years earlier, when then prime minister P.V. Narasimha Rao and then Singapore prime minister Goh Chok Tong mooted the idea of developing infrastructure for the IT industry. Soon after, a consortium led by Ascendas, the Tata Group (which later sold its stake to Ascendas), and the Karnataka Industrial and Area Development Board, which owned the land, started construction on the tech park.

")

View Full Image

An under-construction office space at the International Tech Park Bangalore, operated by CapitaLand Investment. (Madhurima Nandy/Mint)

As India turned into a global IT services outsourcing destination, the Singaporean company steadily built more such tech parks around the country. Today, its footprint has expanded beyond Bengaluru to Chennai, Hyderabad, Pune, Mumbai, and Gurugram. Around 250,000 people work in these parks.

However, because of its measured approach in building its India property business, Ascendas-Singbridge was outpaced by larger and more aggressive US and Canadian investors such as Blackstone Group and Brookfield.

Now, CLI, which has taken over the reins after merging with Ascendas-Singbridge, wants to catch up. In 2024, India constituted around 7% of the company’s funds under management. The goal is to make that at least 10% by 2028.

CLI is 53% owned by Singapore state investor Temasek Holdings. Last year, Temasek, which has directly invested in multiple sectors in the country, said India was its best-performing market.

“India has a lot going for it,” Sanjeev Dasgupta, CEO, CapitaLand Investment India, told Mint. “CLI has ambitious growth targets and expansion plans for the company overall. Given that India is growing so rapidly, CLI wants it to play a bigger part in that growth journey.”

To this end, the company plans to take both the organic and inorganic routes, building from the ground up and making acquisitions. The money for all this will come from CLI’s three capital pools in India. The first is its balance sheet, from which long-gestation projects and land acquisitions are funded. The second is private funds that bring in institutional investors for greenfield developments. And finally, from the Singapore-listed entity CapitaLand India Trust, which focuses on income-generating assets and acts much like a real estate investment trust (Reit).

“The pace of growth will be faster. The way that the office, logistics, and data centre markets have taken off in India, it’s much easier to convince investors today to invest in India-focused funds,” said Dasgupta.

Office expansion

Many global capital providers were in a bit of a wait-and-watch before committing to the office sector in India post pandemic. Now that the sector has picked up, analysts believe investments will pour in from Singapore, Japan and even Korea.

CLI India currently has 13 office parks, spanning 25 million sq. ft, which it owns along with CapitaLand India Trust, the first listed India property trust in Asia, and private fund platforms. Many more are being built—CLI has a development pipeline for 14.3 million sq. ft of office parks, which will come up in the next three-four years across cities to address the demand for premium office spaces.

CLI India currently has 13 office parks, spanning 25 million sq. ft, which it owns along with CapitaLand India Trust, the first listed India property trust in Asia, and private fund platforms.

In 2024, office leasing recorded a historic high of 79 million sq. ft across nine cities, setting a new benchmark for leasing activity, as per property advisory CBRE India data.

Ram Chandnani, managing director, advisory and transaction services, at CBRE India, said that while rupee volatility remains a concern for foreign investors, their expectations on returns have been met in terms of office investments. That is certainly true in the case of CLI. “India is the best-performing office market portfolio in all of CLI. China would always outshine India, but that has changed in the last couple of years,” Gauri Shankar Nagabhushanam, CEO, CapitaLand India Trust, told Mint. “Last year witnessed a record high in office leasing, making India the No. 1 office market in absorption [leasing]. Investors are looking at India more keenly than before.”

Global capability centres (GCC) account for 44% of CLI’s client portfolio in office parks, where it hosts companies such as Amazon, Deloitte, Bristol Myers, Warner Brothers and Xerox, among others. Nagabhushanam said the GCC office leasing momentum will continue to be a major driver for the company.

Last year, the company raised its latest office parks fund, CapitaLand India Growth Fund II ( ₹3,255 crore corpus). New investments in the office segment will be made from this fund, as well as from CapitaLand India Trust.

The logistics bet

As an asset class, India’s office segment has undergone a major shift from standalone buildings to corporate business parks. In warehousing and logistics, however, the move from inefficient to efficient space is still ongoing. So, for institutional investors with a long growth runway, logistics was a natural choice after the office segment.

After developing business parks for close to two decades, Ascendas Firstspace, a logistics and industrial platform born out of a joint venture between Ascendas and Firstspace Realty (India), and now part of CLI, was launched in 2017. Two funds were raised in quick succession to expand the business. In 2018, Ascendas India Logistics Fund raised ₹2,480 crore, and in 2021, CapitaLand India Logistics Fund II raised another ₹2,480 crore.

The timing was just right. The demand for modern warehousing and industrial facilities was growing, thanks to an expansion in manufacturing activity, e-commerce, as well as other sectors. That led to a solid appetite among investors for good quality industrial assets.

In the span of a few years, the platform has emerged as the third largest in the country, after Indospace and Blackstone-owned Horizon Industrial Parks. Ascendas Firstspace has 11 million sq. ft of operational assets, across five facilities. It also has another 13-14 million sq. ft of under-construction projects and projects in the pipeline.

The demand for modern warehousing and industrial facilities is growing, thanks to an expansion in manufacturing activity, e-commerce, as well as other sectors.

So far, the expansion template has been in line with its office parks business strategy: to buy land, and then build and operate warehousing facilities and industrial parks. That could change. To grow faster, large players such as Blackstone are adopting a twin-pronged approach, where they are now building out their portfolio as well as acquiring ready assets to eventually monetize them. Ascendas Firstspace, too, is planning something similar.

“As we expand, we are looking to acquire ready, good-quality assets from other portfolios. We are looking to start that in the next couple of quarters,” said Aloke Bhuniya, CEO, Ascendas Firstspace. “We will do around 3-4 million sq. ft of greenfield development every year. Acquisitions will depend on market conditions and opportunities.”

Like the office sector, India’s logistics and industrial sector recorded an all-time high of 50.4 million sq. ft of net leasing last year, as per property advisory JLL India’s estimates, led by modernization of warehousing and industrial spaces and an increase in demand.

Beyond its core markets of Bengaluru, Chennai, Pune and the Mumbai Metropolitan Region (MMR), Ascendas Firstspace will also enter tier-II markets such as Lucknow and Ahmedabad thanks to rising consumption and disposable income trends making smaller cities attractive for e-commerce players.

E-commerce demand, which peaked in 2021 and then dropped sharply, made a moderate comeback of sorts in 2024. This year will see the return of e-commerce demand in the logistics space, Bhuniya said.

Having built large-format warehousing and industrial facilities, the company also plans to get into new products, such as in-city distribution centres, which are in demand due to the quick commerce boom.

Diversification push

In January, CapitaLand India Trust said it had signed a long-term agreement with a leading global hyperscaler for one of its data centres under development. A hyperscaler is a company that operates a global-scale cloud computing infrastructure.

Data centres, which have emerged as an attractive asset class for institutional investors, are the newest addition to CapitaLand India’s portfolio, a business it set up only in 2021. Globally, it has 27 data centres, to cater to the expansion needs of hyperscalers and enterprises. In India, it has four under development—in Navi Mumbai, Chennai, Hyderabad and Bengaluru—with a total gross power capacity of around 250 megawatts (MW).

After data centres, next in line are renewable energy and private credit for real estate. CLI will enter both these businesses via stake acquisitions, Dasgupta said.

View Full Image

A file photo of Sanjeev Dasgupta, CEO, CapitaLand Investment India.

For renewable energy, which would serve as an adjacency to its own data centres, it is evaluating such platforms or companies for a potential acquisition.

After the 2018 non-banking financial company crisis, there has been a shift in the real estate private credit business, creating space for new private contenders.

“We want to lend to projects at an early stage or those awaiting approvals. We are looking at opportunities to acquire an existing platform. We will put in seed money and raise third-party capital in the new fund management business,” said Dasgupta.

While things look promising, CLI will need to deliver in both existing and new businesses to meet its 2028 growth target. The expansion will also depend on access to capital.

Dasgupta, riding on CLI’s operational expertise over three decades, deep-pocketed sponsor support, and new funds, is brimming with confidence. “The stars have aligned with the market opportunities that have presented themselves in India,” he declared.